The crypto community has a saying: “Not your keys, not your coins,” which means that if you hold your crypto on a third-party custodial wallet, you don’t truly have ownership of the coins. The entity controlling the private key of the wallet ultimately has power over it. Self-hosted wallets, or non-custodial wallets, allow individuals to receive, send and store their own cryptocurrency without the need of a custodial entity.

As life has become increasingly more digitized, the use of cash for transactions and as a store of value has declined considerably. For those in our economy with access to digital resources, online transactions and money services have taken over. However, many individuals stuck in the cash economy do not have the luxury of shopping online or making use of the efficiency of digital transactions.

Related: Americans don’t want to give up their paper money, but they should

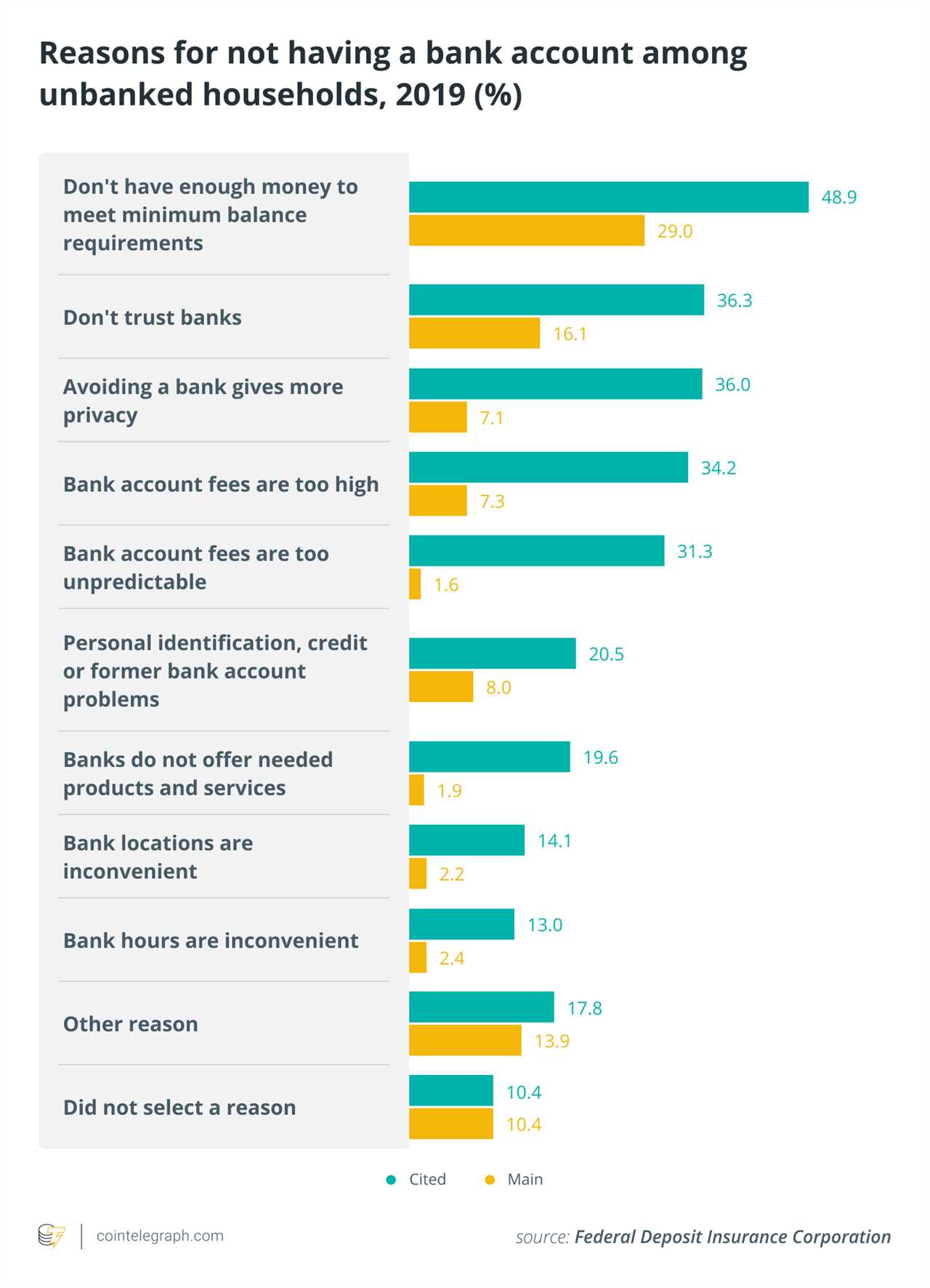

According to the Federal Deposit Insurance Corporation’s 2017 survey of unbanked and underbanked households, approximately 6.5% of households in the United States do not hold an account with an insured financial institution. Almost 19% of households are underbanked, meaning that while they hold at least one account at an insured institution, they still utilize financial products, such as payday loans or cash-checking services. Reasons for these individuals being underbanked can vary from past financial mistakes, a lack of trust in financial institutions, not having enough money for the minimum balance, or wanting to avoid fees. These reasons remained relevant two years later, according to the FIDC’s 2019 survey, where a lack of trust is among the top reasons.

Self-hosted wallets create the value thesis of cryptocurrencies. They allow anyone secure, equal access to a large and growing amount of financial tools, such as DeFi or staking, enabled by blockchain technology. Individuals with these wallets are able to access these tools and securely send money without a third-party intermediary — an impossible feat before the invention of Bitcoin (BTC). These peer-to-peer transactions do not require an intermediary entity because the act of “cutting out the middleman” is what enables the unparalleled efficiency and financial equality that cryptocurrency provides.

By potentially regulating the use of self-hosted wallets, the U.S. government would be creating a barrier for these underbanked and unbanked individuals from accessing cryptocurrency and hindering the greatest catalyst of financial inclusivity the world has ever seen. At the same time, they would also be giving more power to intermediaries in the cryptocurrency space. An internet connection is all that is needed to interact with the global financial system. This is a huge step forward in providing financial freedom to all, making financial services available to the billions who currently lack access. By removing this feature, the government would be rendering cryptocurrency useless to Americans without the specified identification.

Related: How US authorities are using old AML tools to crack down on crypto

In addition, wallets aren’t just digital bank accounts — they’re digital safes. A self-hosted wallet allows people to store all types of digital assets from important documents to tokenized real estate to fiat-tethered cryptocurrencies. Taking away an individual’s right to own their own physical safe would be ludicrous. Taking away the right to own a digital safe is tantamount to an infringement on the rights of Americans.

Cryptocurrency has seen more growth and created more wealth than any other invention in recent history. The U.S. is at the forefront of this boom and has seen immense growth of many companies, the creation of thousands of new jobs and greater financial independence of its citizens as a result. Imposing a regulation that requires wallets to be custodial would put the U.S. behind the eight-ball by stifling innovation and hindering widespread adoption. While other countries continue to use cryptocurrency in its fairest and most streamlined form, the U.S. would be throttling the growth that cryptocurrency’s free market facilitates.

The blockchain ecosystem is still in its infancy, and its true potential hasn’t even been close to realized. Regulating such an important aspect of this new and useful technology would have disastrous repercussions on innovation within the crypto space, likely preventing the future invention of revolutionary products and services that will live on the blockchain.

Related: Friendliest of them all? These could be the best places for crypto

A clear and concise regulatory framework is something the cryptocurrency industry needs, but this is not the approach to take. When creating new regulations, the U.S. government must collaborate with industry professionals and scholars to find a solution that creates strong consumer protections, stimulates innovation and ensures that all cryptocurrency users have secure access to essential financial services.

Title: Rumored US crypto wallet restrictions: A step toward financial exclusion

Sourced From: cointelegraph.com/news/rumored-us-crypto-wallet-restrictions-a-step-toward-financial-exclusion

Published Date: Fri, 18 Dec 2020 17:02:46 +0000