Loans based on cryptocurrencies have become a mainstay of the decentralized finance (DeFi) universe ever since the smart contract-based lending/borrowing platforms began offering the service to crypto users. The Ethereum network, the first blockchain that scaled the smart contract functionality, sees most of the total value locked (TVL) on DeFi protocols dominated by cryptocurrency lending platforms.

According to data from DeFi Pulse, the top 4 of 10 DeFi protocols are lending protocols that account for $37.04 billion in TVL, just 49% of TVL of the entire DeFi market on the Ethereum blockchain. Ethereum leads in terms of being the most utilized blockchain for the DeFi market and the TVL on the network. Maker and Aave are the biggest players here, with a TVL of $14.52 billion and $11.19 billion, respectively.

Even on other blockchain networks like Terra, Avalanche, Solana and BNB Chain, the adoption of cryptocurrency-based loans has been one of the main use cases of smart contracts in the world of DeFi. There are about 138 protocols that provide crypto loan-based services to users, amounting to a total TVL of $50.66 billion, according to DefiLlama. Apart from Aave and Maker, the other prominent players in this protocol category across blockchain networks are Compound, Anchor Protocol, Venus, JustLend, BENQI and Solend.

Johnny Lyu, the CEO of crypto exchange KuCoin, talked to Cointelegraph about the choice of blockchain networks for crypto lending. He said:

“I would say the ideal blockchain for loans and DeFi does not exist, as each has its own advantages. At the same time, the leadership of Ethereum is undeniable due to many factors.”

However, he didn’t negate the possibility of the emergence of a truly ideal blockchain for DeFi. Kiril Nikolov, DeFi strategist at Nexo — a cryptocurrency lending platform — seconded this view. He told Cointelegraph:

“The short answer is ‘no.’ Most blockchains are crypto lending-friendly. However, among the primary properties to watch for are liquidity and reliability, while a secondary determining factor might be network fees.”

Considering that the liquidity and reliability of the Ethereum platform are the highest right now due to it being the most utilized blockchain within DeFi, one could consider taking advantage of the same and making it the blockchain of choice.

Prominent players

To start with, a borrower needs to choose between the major lending protocols on the network such as Maker, Aave and Compound. While there are a plethora of crypto lending platforms, in this piece, the most prominent ones are considered for the sake of ease of explaining and relatability.

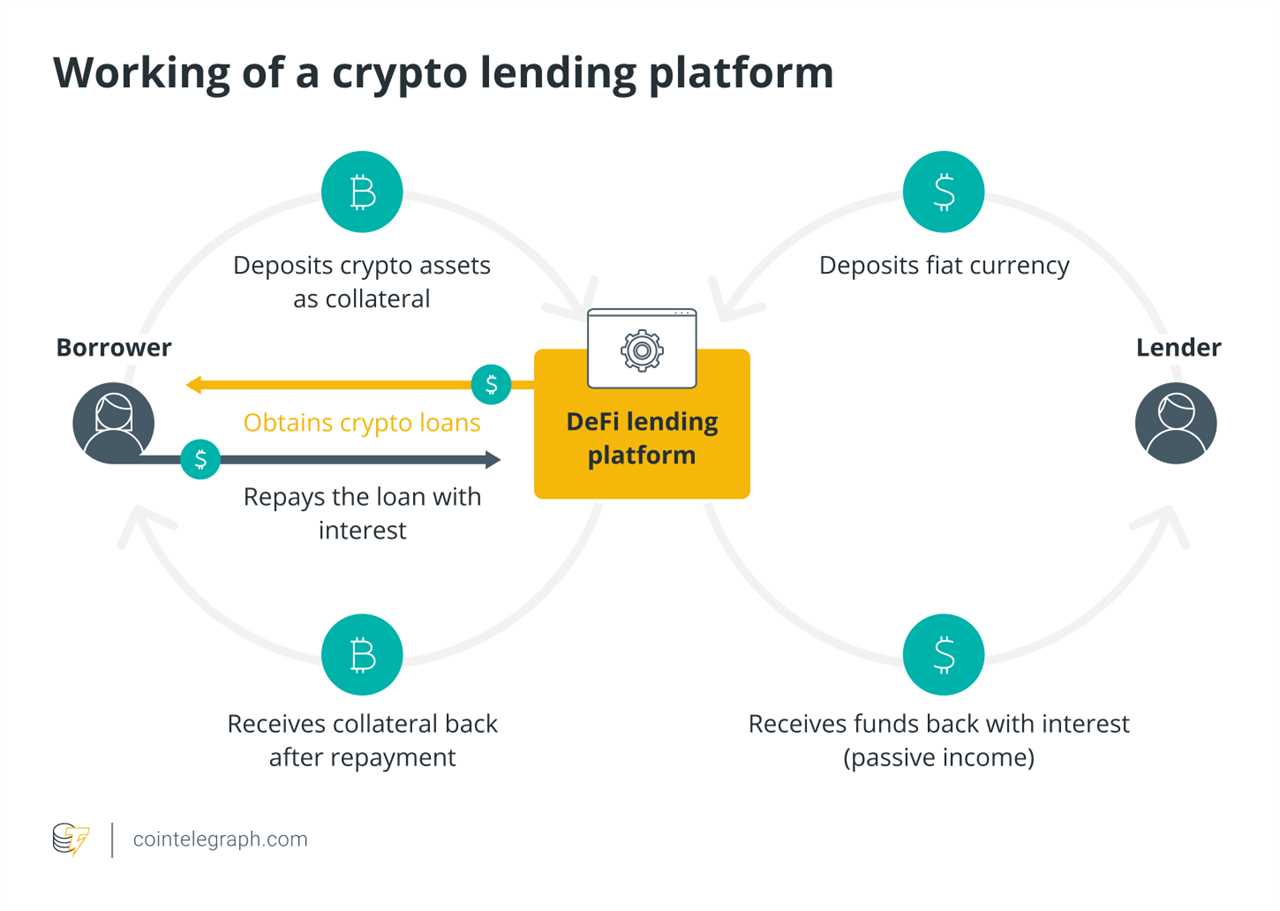

Cryptocurrency lending essentially enables users to borrow and lend digital assets in return for a fee or an interest. Borrowers need to deposit collateral that will instantly allow them to take a loan and use it for the objectives of their portfolio. You can take loans without any collateral, known as flash loans, on platforms like Aave. These loans need to be paid back within the same block transaction and are mainly a feature meant for developers due to the technical expertise required to execute them. Additionally, if the loaned amount is not returned plus the interest, the transaction is canceled even before it is validated.

Since crypto-based loans are completely automated and simple for the average retail investor and market participants, in general, they provide an easy way to earn annual percentage yields on the digital assets they are hodling or even accessing cheap credit lines.

One important aspect of collateralized loans is the loan to value (LTV) ratio. LTV ratio is the measurement of the loan balance in relation to the value of the collateral asset. Since cryptocurrencies are considered to be highly volatile assets, the ratio is usually on the lower end of the spectrum. Considering Aave’s current LTV for Maker (MKR) is 50%, it essentially means that you can borrow only 50% of the value as a loan in relation to the collateral deposited.

This concept exists to provide moving room for the value of your collateral in case it decreases. This results in a margin call where the user is asked to replenish the collateral. If you fail to do so and the value of the collateral falls below the value of your loan or another predefined value, your funds will be sold or transferred to the lender.

The extent of the impact of cryptocurrency-based loans reaches out of the DeFi market since it enables access to capital for individuals or entities without a credit check. This brings a mass population of people across the world that have a bad credit history or no credit history at all. Since lending and borrowing are all driven through smart contracts, there is no real age limit for the younger generation to get involved, which is traditionally not possible through a bank due to the lack of credit history.

Related: What is crypto lending, and how does it work?

Considerations and risks

Since the adoption of DeFi-based loans has now risen to such an extent that even countries like Nigeria are taking advantage of this service and El Salvador is exploring low-interest crypto loans, there are several considerations and risks that are noteworthy for investors looking to dabble in this space.

The primary risk involved with crypto lending is smart contract risk since there is a smart contract in play managing the capital and collateral within each DeFi protocol. One way this risk can be mitigated is by robust testing processes implemented by the DeFi protocols deploying these assets.

The next risk you need to consider is the liquidity/liquidation risk. The liquidity threshold is a key factor here because it is defined as the percentage at which a loan is considered to be under-collateralized and thus leads to a margin call. The difference between LTV and liquidity threshold is the safety cushion for borrowers on these platforms.

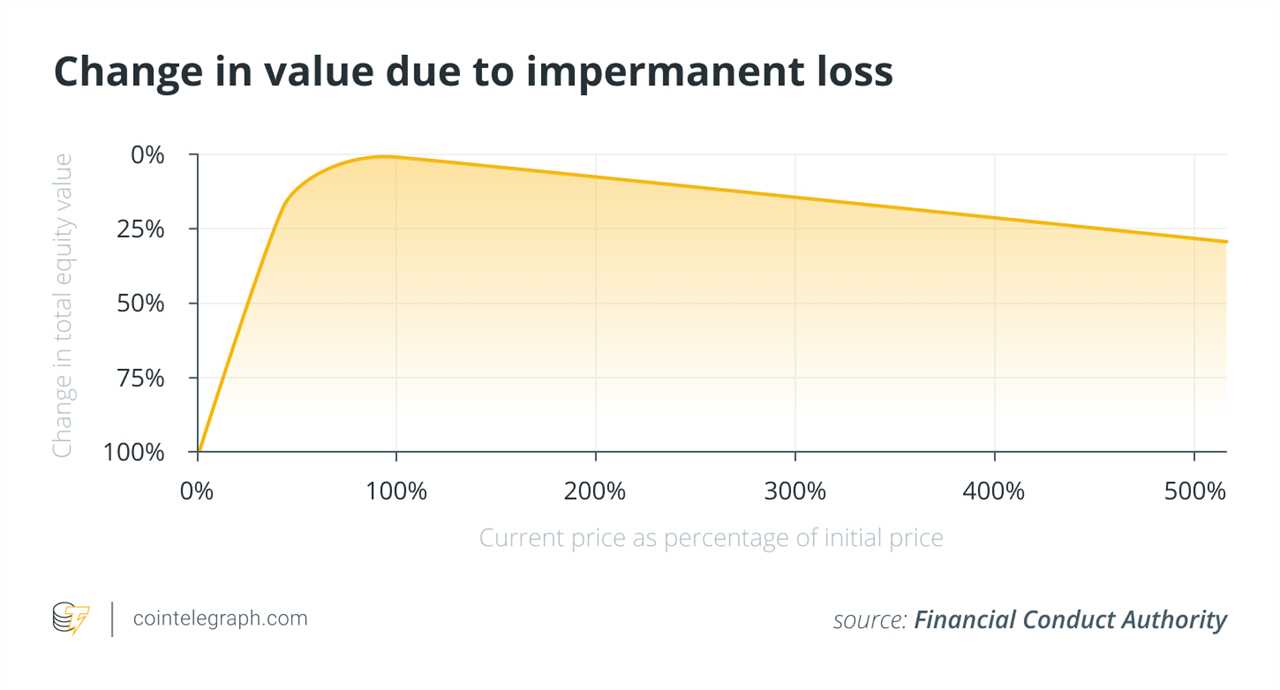

For lenders, there is another additional risk related to impermanent loss. This risk is inherent to the automated market maker (AMM) protocol. This is the loss that you incur when you provide liquidity to a lending pool, and the underlying price of the deposited assets falls below the price at which they were deposited into the pool. However, this only occurs when the fees earned from the pool don’t compensate for this drop in price.

Nikolov pointed out another risk with DeFi lending platforms. He said that “Another one is bad collateral listing which could lead to disturbances of the entire platform. So, if you’re not willing to take these risks, we recommend borrowing from a platform like ours that guarantees you certain protections such as insured custody and over-collateralization.”

There have been several instances of hacks since the increasing popularity of DeFi including Cream Finance, Badger DAO, Compound, EasyFi, Agave and Hundred Finance.

Additionally, cryptocurrency lending and borrowing platforms and users both are subject to regulatory risk. Lyu mentioned that the regulatory framework on this issue has not been fully formed in any major jurisdiction, and everything is changing right before our eyes. It is necessary to separate borrowers from each other — private borrowers and companies of borrowers.

Essentially, the risks highlighted makes it critical for you to exercise extreme caution when deploying your capital in crypto-based loans, either as a borrower or as a lender. Paolo Ardonio, the chief technology officer of crypto exchange Bitfinex, told Cointelegraph:

“It is important that those participating in crypto lending on DeFi platforms be mindful of the risks in what is still a nascent field in the digital token economy. We’ve seen a number of high-profile security breaches that have put the funds of both borrowers and lenders at risk. Unless funds are secured in cold storage, there will inevitably be vulnerabilities for hackers to exploit.”

Recent: Beyond collectibles: How NFTs are revamping the ticketing industry

Future of DeFi lending

Despite the risks mentioned, cryptocurrency-based lending is one of the most evolved spaces in DeFi markets and is still witnessing constant innovation and growth in technology. It is evident that the adoption of this DeFi category is the highest among the numerous others growing in the blockchain industry. The use of decentralized identity protocols could be integrated into these platforms for the verification of users to avoid the entry of scrupulous players.

Ardonio spoke further on the innovation expected in DeFi loans this year, stating, “I expect to see more innovation in crypto lending, particularly in terms of the use of digital tokens and assets as collateral in loans. We are even seeing nonfungible tokens being used as collateral in loans. This will be an emerging trend this year.”

Title: Looking to take out a crypto loan? Here’s what you need to know

Sourced From: cointelegraph.com/news/looking-to-take-out-a-crypto-loan-here-s-what-you-need-to-know

Published Date: Sun, 24 Apr 2022 15:09:00 +0100